Tyranny of the Arbitrators -

And the End of Small Claims Court

After a minor banking dispute in 2010 forced me to file a small claim, Citibank removed my small claim to private arbitration against my objections and in violation of my agreements and the arbitrator’s rules.I am sharing my story to help others...

Citibank removed my small claim to arbitration to avoid an undesirable but public outcome in small claims court — knowing full well the depth of the hole it was putting me in.

Tyranny of the Arbitrators And the End of Small Claims Court

I banked with Citibank for years. While an employee of Citigroup’s investment bank, I opened consumer bank accounts in 2007 before leaving in 2009. After a minor banking dispute in 2010 forced me to file a small claim, Citibank removed my small claim to private arbitration against my objections and in violation of my agreements and the arbitrator’s rules.

I am sharing my story to help others. While I get into some technical detail, I hope that non-technical readers can skim past it and still understand the issue.

This is my — and only my — opinion.

I am not a lawyer — and that’s really the point.

To keep this relatively short, I will detail my underlying dispute in a forthcoming post.

It is entirely possible that Citibank removed my small claim to arbitration to avoid an undesirable but public outcome in small claims court — knowing full well the depth of the hole it was putting me in.

The Dispute

Citibank wrongfully charged me late fees and harmed my credit in 2010. I have always had excellent credit and have repeatedly leveraged it to take advantage of opportunities. After a lengthy but unsuccessful attempt at resolving my dispute with Citibank from 2010–2012, I filed for small claims court in Pima County, Arizona (Tucson metro) in January 2012[1].

I requested “the refund of $289.50 in account fees, $50.00 in late fees, $2,060.50 in compensation for my time and efforts, and a correction to all of my credit reports.â€[2]

I represented myself, or what is known in the legal world as “pro se representation.â€

An Arizona small claims court cannot grant compensation for “time and efforts†nor can it directly command a party to correct another’s credit report (injunctive relief). The court can determine if Citibank wrongfully charged me fees and, under the Fair Credit Reporting Act (“FCRAâ€), after such a determination, Citibank would be obligated to correct my credit reports. If Citibank failed to do so, I could then seek further relief directly or through the credit reporting agencies (“CRAsâ€).

So, to an expert eye, my small claim boiled down to $339.50 in fees.

The Citibank Arbitration Agreement Checking Plus Agreement, September 1, 2010. Page 4 of 6.

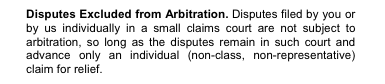

I read our arbitration agreement, particularly the excerpted clauses included here, and interpreted them to mean that small claims court disputes were excluded from arbitration[3].

I filed a small claim.

Shortly after my filing, Citibank filed a motion to remove my small claim to arbitration: “Citibank affirmatively alleges that the Checking Plus Account Agreement …[is] subject to mandatory arbitration pursuant to the terms of arbitration clauses in the Agreements, and pursuant to the Federal Arbitration Act, 9 U.S.C. 2 et seq., and/or Arizona law.â€[4]

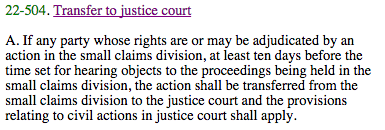

Arizona Revised Statutes (“A.R.S.â€) 22–504 allows either party to a small claim tounilaterally (meaning without any other party’s consent) remove it to a higher court by written request. This request is not reviewed. It is automatically and immediately granted by statute.

In its motion, Citibank simultaneously:

cited A.R.S. 22–504 to unilaterally and automatically have my small claim removed to Justice Court; and,

cited the arbitration agreement’s

Disputes Excluded from Arbitrationclause

—

“…so long as the disputes remain in [small claims] court…â€

—

to force this newfound Justice Court case into mandatory arbitration.

By unilaterally removing my small claim from small claims court, Citibank had exposed its agreement to contain a deceptive trap that does not grant a right to small claims court.

Small claims disputes are not excluded from mandatory arbitration.

Needless to say, this caught me by surprise. Why would Citibank want to make resolution more time consuming, expensive and complicated?

Under A.R.S. 22–512(d), attorneys can represent in Arizona small claims court. So that could not have been the issue.

As a non-lawyer, when I read the clause “…so long as the disputes remain in [small claims] court…â€, I interpret it to mean that I, as the consumer-plaintiff, cannot avoid arbitration by filing a small claim only to unilaterally remove it to a higher court and claim that my dispute is not subject to arbitration because it originated in small claims court.

As such, I interpret its construction to be defensive — to prevent procedural abuses by the consumer. The problem is that Citibank did not invoke it defensively, it invoked it offensively — to abuse or take advantage of the procedures at the expense of the consumer.

Used offensively, the clause is unfair and deceptive. It is unlikely that any consumer will read the arbitration agreement and conclude that they must first get Citibank’s permission to proceed in small claims court.

What advantages did Citibank gain?

Secrecy: arbitrations are private and small claims court is not.

Extension: Citibank gets to extend its war of attrition against small claimants. Arbitration is a more expensive, foreign and time-consuming process than a small claims court likely leading to a discouraged attitude of, “Oh, to Hell with it!â€

Procedural-Technical-Legal Morass: Small claims court is a purposely expedited hearing format. Arbitration, like regular court, is subject to all sorts of legal gamesmanship, procedure and delay.

In my experience, the arbitrator selection process takes more time than the entirety of small claims court resolution.

After exhausting my ability to object in Justice Court, the judge ultimately ordered my small claim to arbitration seemingly on the basis of the removal portion of the

Disputes Excluded from Arbitration clause.

Justice Court order compelling arbitration, October 24, 2012Justice Court clarification on removal, November 10, 2012

If Citibank intends to arbitrate small claims, why not simply say so? Why mislead customers into believing small claims are excluded?

Who else is Citibank deceiving?

The Arbitrator’s Rules

Our arbitration agreement — like most others — names the American Arbitration Association (“AAAâ€) and JAMS (not an acronym) as my choices of arbitrator.

The AAA and JAMS have similar rules requiring consumers have access to small claims court. I ultimately chose the AAA because of its more extensive consumer documentation and its “Consumer Due Process Protocol.â€[5]

Excerpt from “AAA Review of Consumer Clausesâ€, page 1, AAA Online LibraryExcerpt from “AAA Review of Consumer Clausesâ€, page 1, AAA Online Library

One of the documents that the AAA provided me is called the “AAA Review of Consumer Clauses.â€[6] Not only does it state that I have a “Small Claims Court Optionâ€, it states that arbitration clauses failing to meet fairness standards contained in the AAA’s Consumer Due Process Protocol (“CDPPâ€) will be denied access to the AAA’s services.

So the AAA has seemingly established the CDPP as a standard for judging fairness, at a minimum.

Let’s review the CDPP.

Principle 5 and Reporter’s Comments from the AAA’s “Consumer Due Process Protocolâ€, page 18, AAA Online LibraryLet’s review the CDPP.Principle 11 from the AAA’s “Consumer Due Process Protocolâ€, page 3, AAA Online LibraryLet’s review the CDPP.

There are two principles that appear most relevant to my experience: Principles 5 and 11.

Principle 5 requires Citibank’s arbitration agreement “make it clear that all parties retain the right to seek relief in a small claims court.â€

Principle 11(c) reinforces Principle 5 by requiring Citibank to give me notice of my right to small claims court.

Excellent, right? The AAA is most assuredly going to deny its services by determining Citibank’s arbitration agreement and actions fundamentally unfair and non-compliant with the CDPP.

Excerpt from “Supplementary Procedures for the Resolution of Consumer-Related Disputesâ€, page 4, AAA Online LibraryRule C-1(d) from the “Supplementary Procedures for the Resolution of Consumer-Related Disputesâ€, page 8, AAA Online Library

Just to be sure, let’s look at the AAA’s “Supplementary Procedures for the Resolution of Consumer-Related Disputes.â€[7]

The introduction to the Supplementary Procedures mirrors the CDPP and Rule C-1(d) says parties can take their claims to a small claims court.

Great.

Excerpt from “Supplementary Procedures for Consumer-Related Disputes Questions and Answersâ€, page 1, AAA Online Library

Furthermore, a Q&A document (excerpted here) that is included with the Supplementary Procedures states that I cannot be contractually barred from small claims court[8].

By incorporating the AAA into its agreement, Citibank waived its right to unilaterally invoke A.R.S. 22–504 to transfer a small claim to Justice Court for the purpose of compelling arbitration. Invoking that waived right was to foreclose its access to the AAA’s services.

After all, the AAA’s rules are clear that consumers cannot be prohibited from seeking relief in a small claims court. I was prohibited so Citibank will suffer the consequences.

Nope.

The AAA’s Lack of Internal Controls

As a self-represented plaintiff, I was at a significant disadvantage against Citibank’s repeated appeals to technical legal and procedural arguments.

For my protection, I decided to retain counsel.

We filed an initial brief with our AAA Demand for Arbitration that summarized the underlying dispute as well as the rule-violating removal of my small claim.

The AAA is supposed to perform an “intake review†of any claim to determine which subcontractor-arbitrator is the best fit. Because it was never disclosed otherwise, we presumed the arbitrator was to decide the small claims removal issue.

Much later, after going through a lengthy arbitrator selection process (in my view, arbitrator shopping by Citibank), some hearings and a ruling on the removal issue, it came to my attention that the AAA should have determined Citibank’s arbitration agreement non-compliant during the intake review process.

Ironically, comments made by Citibank’s counsel tipped us off to this fact.

As such, the AAA abdicated its duty to perform reasonable due diligence. It did not ask for supporting documentation or ask any follow up questions during the intake review process. As a result, we went through a year-plus of superfluous proceedings and expense.

Furthermore, by failing to review the question, or by reviewing the question and still deciding Citibank’s arbitration agreement and actions were fair and compliant, the AAA had put their subcontracted arbitrator in the position of having to rule against the AAA — his employer — in order to find against Citibank.

What employee is going to make a consequential ruling against his employer? It is a massive conflict of interest. Do you sacrifice your future relationship with the AAA over a rules violation by Citibank — surely one of the AAA’s largest customers as one of the world’s largest banks?

The ruling was as bizarre as one would expect under such a scenario.

Indifference Favors the Wrongdoer

During the summer 0f 2014, immediately after discovering the AAA’s abdication of duty, I wrote the professional staff at the AAA to find out why this important step in the process was negligently disregarded and not disclosed.

Why did we waste a bunch of time finding and presenting to an arbitrator when it was the AAA’s decision to make?

Why was there not a process in place to address these questions and safeguard against negligence?

Why am I piecing this together through comments by Citibank’s counsel and not AAA disclosures?

The AAA’s staff made artful attempts to invent disqualifying preconditions but ultimately failed to satisfy key questions.

The AAA framed it as two choices:

deny its services; or

require a party’s already-removed claim to still fit small claims jurisdiction in order to deny its services.

How the AAA gets past 1 to 2 is beyond me. Removal is supposed to cause a denial of services — not removal with a precondition that it can be returned. Otherwise a wrongdoer can always remove and bet on a consumer’s ignorance or that post-removal changes and accrued costs will exceed small claims court jurisdiction thus preventing return.

By the very order of process, a post-removal small claim has both increased expense and increased access to relief. The reasonable act of hiring an attorney post-removal prices the claim out of small claims court ($3,500 current limit in Pima County, Arizona) — especially if any work has been done.

The AAA is seemingly creating an anti-consumer catch-22 that it has no business forming. Indeed, this artificial catch-22 is in contradiction to the very documents that the AAA provides consumers.

Notably, in September 2014, a few months after my exchange with the AAA, the AAA unveiled amended “Consumer Arbitration Rules†that included detailed procedures on how to access small claims court[9].

The new Consumer Arbitration Rules also include Rule R-1(d), which reinforces the AAA’s long held obligation to refuse to accept claims that do not “meet the due process standards contain in the

Consumer Due Process Protocol.â€

While this is an important first step, it does not prevent what happened to me from happening to others.

I acted upon my right to small claims court, as one would under the new Rule R-9(a), and it was

still removed to arbitration.

The AAA’s indifference favors Citibank, the wrongdoer.

The AAA must deny its services to unilaterally-removed small claims. It must not allow them to get past the intake review process.

If the AAA does not practice reasonable due diligence, many more consumers are going to be tied up for years with unnecessary and wasteful arbitration proceedings for their

small claims.

I filed my small claim in January 2012. It is March 2015 and we are still in arbitration. Small claims would have been completed by May 2012, at the latest.

Citibank has undoubtedly spent close to if not more than one hundred thousand dollars on fighting my small claim. Its external counsel does not come cheap[10].

Ambiguity has to be interpreted against the interests of the drafting party. An impartial review of the AAA’s rules would surely lead one to conclude that the AAA was supposed to deny its services to Citibank. Not doing so effectively makes the AAA’s rules meaningless.

Is Citibank making a mockery of the AAA?

Are Citibank and the AAA in cahoots?

Is it a marriage of choice or one of convenient indifference?

I am Not a Lawyer — and Should Not Have to Be

A big motivation for sharing my experience is to protect others. The next time a consumer is subject to a similar situation, hopefully they will find my story through a Google search and be starting from a more informed position.

Why did Citibank remove my claim from a court with a maximum theoretical liability of $2,500 (at the time; it is now $3,500) when the cost of removal surely exceeded that?

Why did the AAA allow a unilaterally-removed small claim into arbitration?

For now, I have more questions than answers. One of these days I’ll provide an update with more answers than questions.

I certainly did not seek or expect this fight. Citibank and the AAA drafted me into it. I have put more time, resources and stress into it than I will ever get back. My fight has transformed into a larger fight for the public good — a rare silver lining in this ridiculous nightmare.

It was never about the $339.50 in fees. All I ever cared about was my credit. I hoped that the mere act of filing a small claim would cause Citibank to fix my credit because the cost of doing so was miniscule.

I could not have been more wrong.

Small claims are not excluded from mandatory arbitration.

I am not a lawyer — and that’s really the point.

If you find yourself in a similar situation, be sure to get the latest documents from the AAA or JAMS. The AAA will undoubtedly be phasing out some of the documents that I have cited, if they have not already.

Please reach out to me with any questions or if you would like to help. Small claims court is an important institution for expedient and affordable dispute resolution. It should never be substituted by arbitration without mutual consent and there should be real consequences for abusing procedure.

Footnotes:

[1] I opened Citibank consumer checking and overdraft accounts in 2007 in New York, New York. I currently live in Tucson, AZ and have since 2009.