|

Report Mortgage Fraud: WWW.NAMB.org

FINANCIAL CRIMES REPORT TO THE PUBLIC

MORTGAGE FRAUD - MAY 2005

The increased reliance by both financial institutions and non-financial institution lenders on third-party brokers has created opportunities for organized fraud groups, particularly where mortgage industry professionals are involved.

**********************************************************************

U. S. Department of Justice

Federal Bureau of Investigation

| FINANCIAL CRIMES SECTION | CRIMINAL INVESTIGATIVE DIVISION |

FINANCIAL CRIMES REPORT TO THE PUBLIC

MORTGAGE FRAUD

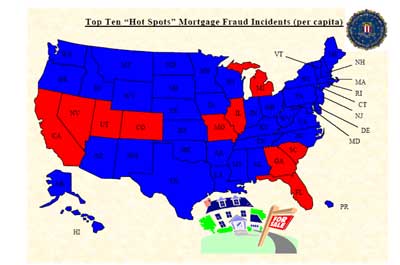

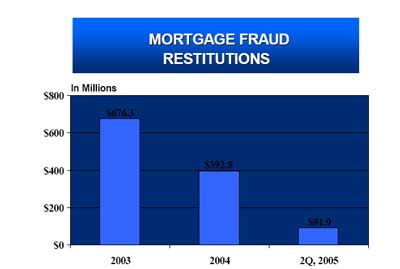

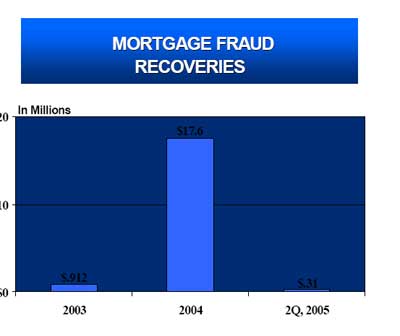

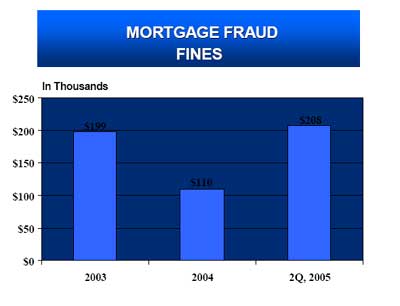

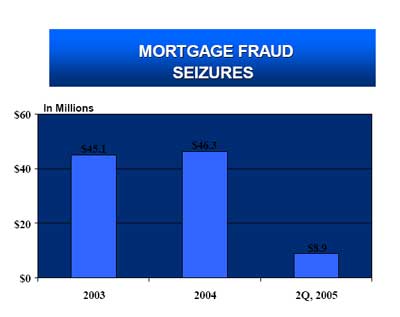

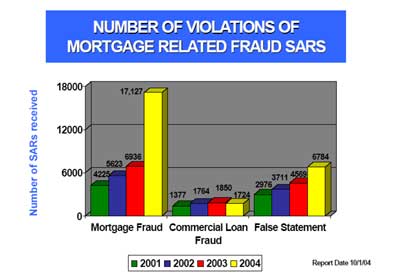

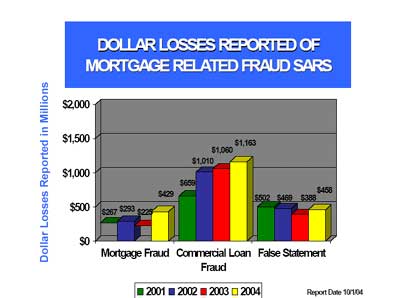

I. General OverviewThe increased reliance by both financial institutions and non-financial institution lenders on third-party brokers has created opportunities for organized fraud groups, particularly where mortgage industry professionals are involved. Combating significant fraud in this area is a priority, because mortgage lending and the housing market have a significant overall effect on the nation's economy. All mortgage fraud programs were recently consolidated within the Financial Institution Fraud Unit, even where the targeted lender is not a financial institution. This consolidation provides a more effective and efficient management over mortgage fraud investigations, the ability to identify and respond more rapidly to emerging mortgage fraud problems, and a better picture of the overall mortgage fraud problem. Each mortgage fraud scheme contains some type of "material misstatement, misrepresentation, or omission relied upon by an underwriter or lender to fund, purchase or insure a loan." The Mortgage Bankers Association projects $2.5 trillion in mortgage loans will be made during 2005. The FBI compiles data on mortgage fraud through Suspicious Activity Reports (SARs) filed by federally-insured financial institutions, and Department of Housing and Urban Development Office of Inspector General (HUD-OIG) reports. The FBI also receives complaints from the mortgage industry at large. A significant portion of the mortgage industry is void of any mandatory fraud reporting. In addition, mortgage fraud in the secondary market is often under reported. Therefore, the true level of mortgage fraud is largely unknown. The mortgage industry itself does not provide estimates on total industry fraud. Based on various industry reports and FBI analysis, mortgage fraud is pervasive and growing. The FBI investigates mortgage fraud in two distinct areas: Fraud for Profit and Fraud for Housing. Fraud for Profit is sometimes referred to as "Industry Insider Fraud" and the motive is to revolve equity, falsely inflate the value of the property, or issue loans based on fictitious properties. Based on existing investigations and mortgage fraud reporting, 80 percent of all reported fraud losses involve collaboration or collusion by industry insiders. Fraud for Housing represents illegal actions perpetrated solely by the borrower. The simple motive behind this fraud is to acquire and maintain ownership of a house under false pretenses. This type of fraud is typified by a borrower who makes misrepresentations regarding his income or employment history to qualify for a loan. The defrauding of mortgage lenders should not be compared to predatory lending practices which primarily affect borrowers. Predatory lending typically effects senior citizens, lower income and challenged credit borrowers. Predatory lending forces borrowers to pay exorbitant loan origination/settlement fees, sub-prime or higher interest rates, and in some cases, unreasonable service fees. These practices often result in the borrower defaulting on his mortgage payment and undergoing foreclosure or forced refinancing. Although there are many mortgage fraud schemes, the FBI is focusing its efforts on those perpetrated by industry insiders. The FBI is engaged with the mortgage industry in identifying fraud trends and educating the public. Some of the current rising mortgage fraud trends include: equity skimming, property flipping, and mortgage related identity theft. Equity skimming is a tried and true method of committing mortgage fraud. Today's common equity skimming schemes involve the use of corporate shell companies, corporate identity theft, and the use or threat of bankruptcy/foreclosure to dupe homeowners and investors. Property flipping is nothing new; however, once again law enforcement is faced with an educated criminal element that is using identity theft, straw borrowers and shell companies, along with industry insiders to conceal their methods and override lender controls. Property flipping is best described as purchasing properties and artificially inflating their value through false appraisals. The artificially valued properties are then repurchased several times for a higher price by associates of the "flipper." After three or four sham sales, the properties are foreclosed on by victim lenders. Often flipped properties are ultimately repurchased for 50 - 100 percent of their original value. Since 1999, the FBI has been working to actively investigate mortgage fraud in various cities across the United States. The FBI also focuses on fostering relationships and partnerships with the mortgage industry to promote mortgage fraud awareness. To raise awareness of this issue and provide easy accessibility to investigative personnel, the FBI has provided points-of-contacts to relevant groups including the Mortgage Bankers Association (MBA), the Mortgage Asset Research Institute, the Mortgage Insurance Companies of America, Fannie Mae, Freddie Mac, and others. The FBI has also been working to establish broader SAR reporting requirements for mortgage lenders who do have adequate protection under the current safe harbor provisions. The FBI is collaborating with the mortgage industry and Financial Crimes Enforcement Network to create a more productive reporting requirement for mortgage fraud. The FBI has also been working with the mortgage industry through the MBA to promote a more efficient and effective method of identifying and reporting fraudulent mortgage activity, otherwise known as, the Suspicious Mortgage Activity Report (SMARt Form) concept. The FBI works closely with individual lenders, as well as national associations such as the MBA, the Appraisal Institute, the National Association of Mortgage Brokers, and the National Notary Association, to define and combat the mortgage fraud problem. In addition, on a case-by-case basis, the FBI receives close cooperation from lenders. An example of this is the usage of Real Estate Owned properties from lender inventories to facilitate mortgage fraud undercover operations (UCO). In December 2003, the FBI initiated an UCO to address the massive amount of mortgage fraud in the Jacksonville area. On September 16, 2004, as a result of this investigation, seven search warrants were executed and two arrests were made. Mortgage broker J.R. Parker and closing attorney Dale Beardsley, were arrested via complaint, charging them with bank fraud for their role in this alleged scheme. This UCO was made possible by the close cooperation of a local financial institution. This type of cooperation happens around the country and is a key component in the FBI's approach to this growing crime problem. A recent analysis of mortgage industry fraud surveys identified 26 different states as having significant mortgage fraud problems. Although every survey identified Georgia and Florida as having significant mortgage fraud related investigations, the survey also identified nine other states in the South and Southwest, seven states in the West and five states in the Midwest as having mortgage fraud problems. II. Overall Accomplishments

II. Significant Cases

REO FLIPWAGON (JACKSONVILLE): In December 2003, the FBI initiated an UCO to address the massive amount of mortgage fraud in the Jacksonville area. On September 16, 2004, as a result of this investigation, seven search warrants were executed and two arrests were made. Mortgage broker J. R. Parker and closing attorney Dale Beardsley, were arrested via complaint, charging them with bank fraud for their role in this alleged scheme.

OPERATION CLEAN DEED (CHARLOTTE): In November 2002, an FBI UCO was initiated utilizing a cooperating witness to introduce undercover FBI Agents into seven organizations involved in a multimillion-dollar mortgage fraud ring. Investigation led to the identification of fraudulent loans which exposed financial institutions and mortgage companies to potential losses of $130 million. On September 16, 2004, informations were filed in U.S. District Court, Western District of North Carolina, charging six individuals with bank fraud for their roles in a multimillion-dollar mortgage fraud. JAMES MCLEAN; PRESIDENT; ET AL; FIRST BENEFICIAL MORTGAGE COMPANY - VICTIM (CHARLOTTE): A two-year joint investigation by the FBI, the Internal Revenue Service, and HUD-OIG revealed a fraud for profit scheme committed by several insiders of First Beneficial Mortgage Corporation. This two-year fraud was perpetrated against Fannie Mae and Ginnie Mae home loan programs resulting in losses exceeding $30 million. Recently, the president of First Beneficial Mortgage Corporation and six others were convicted on conspiracy, bank fraud, wire fraud, and money laundering charges. The president was sentenced to 21 years in prison, order to pay $23 million in restitution and forfeited about $8 million in property. MAGGIE CUEVAS; FAG-HUD; FIF (LOS ANGELES): A joint investigation conducted by the Los Angeles FBI Office and HUD-OIG illustrated an extensive scheme in which fraudulent identification and employment documents were used to perpetrate mortgage frauds. The scheme was largely assisted by an individual who regularly manufactured false identity and income documents for a profit. This document forger created W-2s, pay stubs, credit letters and social security printouts over an eight-year period. These documents were used by real estate professionals who knowingly submitted the falsified information to lending institutions. The loans were then insured by HUD and caused a loss to that agency of more than $18 million. A search warrant executed during the investigation revealed more than 100 real estate professionals had ordered false documents in the past. To date, the document forger and six associates have been convicted in the scheme, as well as 14 real estate professionals.

BRENT BARBER dba MIDTOWNE RESTORATION, L.L.C (KANSAS CITY): A two-year joint investigation conducted by the Kansas City FBI Office, IRS, and HUD-OIG culminated on August 13, 2004 with the arrest of Brent Barber, real estate investor. Barber, along with his three business associates were charged in U.S. District Court for their alleged roles in purchasing run-down properties, securing fraudulent appraisals, and obtaining mortgages in the names of straw purchasers. It is alleged that the straw purchasers were paid $2,000 for their role in the scheme whereby they placed properties in foreclosure, leaving Barber and his associates with the mortgage proceeds. This scenario was repeated approximately 300 times, resulting in losses to lending and financial institutions in excess of $15 million. MORTGAGE FRAUD INDICATORSInflated Appraisals

• Exclusive use of one appraiser Increased Commissions/Bonuses - Brokers and Appraisers

• Bonuses paid (outside or at settlement) for fee-based services

• Higher than customary fees Falsifications on Loan Applications

• Buyers told/explained how to falsify the mortgage application

• Requested to sign blank application Fake Supporting Loan Documentation

• Requested to sign blank employee or bank forms

• Requested to sign other types of blank forms Purchase Loans Disguised as Refinance

• Purchase loans that are disguised as refinances

requires less documentation/lender scrutiny Investors-Short Term Investments with Guaranteed Re-Purchase

• Investors used to flip property prices for fixed percentage

• Multiple "Holding Companies" utilized to increase

property values

COMMON MORTGAGE FRAUD SCHEMESProperty Flipping - Property is purchased, falsely appraised at a higher value, and then quickly sold. What makes property illegal is that the appraisal information is fraudulent. The schemes typically involve one or more of the following: fraudulent appraisals, doctored loan documentation, inflating buyer income, etc. Kickbacks to buyers, investors, property/loan brokers, appraisers, title company employees are common in this scheme. A home worth $20,000 may be appraised for $80,000 or higher in this type of scheme. Silent Second - The buyer of a property borrows the down payment from the seller through the issuance of a non-disclosed second mortgage. The primary lender believes the borrower has invested his own money in the down payment, when in fact, it is borrowed. The second mortgage may not be recorded to further conceal its status from the primary lender. Nominee Loans/Straw Buyers - The identity of the borrower is concealed through the use of a nominee who allows the borrower to use the nominee's name and credit history to apply for a loan. Fictitious/Stolen Identity - A fictitious/stolen identity may be used on the loan application. The applicant may be involved in an identity theft scheme: the applicant's name, personal identifying information and credit history are used without the true person's knowledge. Inflated Appraisals - An appraiser acts in collusion with a borrower and provides a misleading appraisal report to the lender. The report inaccurately states an inflated property value. Foreclosure Schemes - The perpetrator identifies homeowners who are at risk of defaulting on loans or whose houses are already in foreclosure. Perpetrators mislead the homeowners into believing that they can save their homes in exchange for a transfer of the deed and up-front fees. The perpetrator profits from these schemes by remortgaging the property or pocketing fees paid by the homeowner. Equity Skimming - An investor may use a straw buyer, false income documents, and false credit reports, to obtain a mortgage loan in the straw buyer's name. Subsequent to closing, the straw buyer signs the property over to the investor in a quit claim deed which relinquishes all rights to the property and provides no guaranty to title. The investor does not make any mortgage payments and rents the property until foreclosure takes place several months later. Air Loans - This is a non-existent property loan where there is usually no collateral. An example of an air loan would be where a broker invents borrowers and properties, establishes accounts for payments, and maintains custodial accounts for escrows. They may set up an office with a bank of telephones, each one used as the employer, appraiser, credit agency, etc., for verification purposes. Mortgage Fraud Prevention Measures General Fraud Tips Mortgage Fraud is a growing problem throughout the United States. People want to believe their homes are worth more than they are, and with housing booms going on throughout the U.S., there are people who try to capitalize on the situation and make an easy profit. Tips to protect you from becoming a victim of Mortgage Fraud • Get referral for real estate and mortgage professionals. Check the licenses of the industry professionals with state, county, or city regulatory agencies.

• If it sounds too good to be true, it probably is. An outrageous promise of extraordinary profit in a short period of time signals a problem.

• Be wary of strangers and unsolicited contacts, as well as high-pressure sales techniques.

• Look at written information to include recent comparable sales in the area, and other documents such as tax assessments to verify the value of the property.

• Understand what you are signing and agreeing to--If you do not understand,

re-read the documents, or seek assistance from an attorney.

• Make sure the name on your application matches the name on your identification.

• Review the title history to determine if the property has been sold multiple times within a short period--It could mean that this property has been "flipped" and the value falsely inflated.

• Know and understand the terms of your mortgage--Check your information against the information in the loan documents to ensure they are accurate and complete.

• Never sign any loan documents that contain blanks--This leaves you vulnerable to fraud.

• Check out the tips on the Mortgage Bankers Association's (MBA) website at http://www.StopMortgageFraud.com for additional advice on avoiding mortgage fraud. Mortgage Debt Elimination Schemes• Be aware of e-mails or web-based advertisements that promote the elimination of mortgage loans, credit card and other debts while requesting an up-front fee to prepare documents to satisfy the debt. The documents are typically entitled Declaration of Voidance, Bond for Discharge of Debt, Bill of Exchange, Due Bill, Redemption Certificate, or other similar variations. These documents do not achieve what they purport.

• There is no magic cure-all to relieve you of debts you incurred.

• Borrowers may end up paying thousands of dollars in fees without the elimination or reduction of any debt.

Foreclosure Fraud SchemesPerpetrators mislead the homeowners into believing that they can save their homes in exchange for a transfer of the deed, usually in the form of a Quit-Claim Deed, and up-front fees. The perpetrator profits from these schemes by remortgaging the property or pocketing fees paid by the homeowner without preventing the foreclosure. The victim suffers the loss of the property as well as the up-front fees. • Be aware of offers to "save" homeowners who are at risk of defaulting on loans or whose houses are already in foreclosure.

• Seek a qualified Credit Counselor or attorney to assist.

Predatory Lending Schemes • Before purchasing a home, research information about prices of homes in the neighborhood.

• Shop for a lender and compare costs. Beware of lenders who tell you that they are your only chance of getting a loan or owning your own home.

• Beware of "No Money Down" loans--This is a gimmick used to entice consumers to purchase property that they likely cannot afford or are not qualified to purchase. Be wary of mortgage professional who falsely alter information to qualify the consumer for the loan.

• Do not let anyone convince you to borrow more money than you can afford to repay.

• Do not let anyone persuade you into making a false statement such as overstating your income, the source of your down payment, or the nature and length of your employment.

• Never sign a blank document or a document containing blanks.

• Read and carefully review all loan documents signed at closing or prior to closing for accuracy, completeness and omissions.

• Be aware of cost or loan terms at closing that are not what you have agreed to.

• Do not sign anything you do not understand.

• Be suspicious if the cost of a home improvement goes up if you accept the contractor's financing.

• If it sounds too good to be true--it probably is! See full report on Financial Crimes

http://www.fbi.gov/publications/financial/fcs_report052005/fcs_report052005.htm#c1

|